Wall Street is currently punishing one of the most powerful companies in artificial intelligence.

A company sitting on hundreds of billions of dollars in contracted revenue, directly tied to the AI infrastructure boom — and the market has cut its stock nearly in half.

Most investors panic when they see a chart like that. Most investors run for the exits.

But sometimes, absolute market panic is exactly when you should start paying attention. Behind the scenes, this company is quietly building something that could secure one of the most dominant positions in the entire AI economy.

Most people looking at this stock right now think the story is over.

I think the story is just getting started.

The AI Bloodbath Everyone Is Misreading

The company I’m targeting has taken a 58% thrashing in the last six months alone.

When a major tech player loses more than half its value in half a year, the consensus is usually that the business model is permanently broken. Investors see red on their screens, stop asking questions, and just hit the sell button.

But to understand why this massive selloff is actually a rare opportunity, you have to understand a fundamental shift happening in artificial intelligence right now — one that almost nobody in the mainstream financial media is talking about correctly.

Everyone assumes the future of AI is entirely about the models.

- ChatGPT

- Gemini

- Grok

- Llama

Billions of dollars are being poured into GPUs, training clusters, and massive data centers just to power these models.

But billionaire Larry Ellison recently shared an insight that completely changes the math on this sector.

Why AI Models May Become Commodities

Ellison pointed out a glaring flaw in the current AI gold rush.

All of these massive, multi-billion-dollar AI models are training on the exact same data. They’re scraping the public internet. They’re absorbing Wikipedia. They’re reading Reddit. They’re processing the exact same news articles and public websites.

Think about the logical conclusion of that process.

So if the models eventually become commodities, what becomes the actual competitive advantage?

The True AI Moat: Private Data

If public data makes AI models identical, the real moat becomes private data.

This is the information that never touches the public internet. It’s the data locked away behind corporate firewalls and high-level security clearances.

- The financial records inside banks

- The medical histories inside hospitals

- The operational data inside Fortune 500 companies

If artificial intelligence shifts toward private data — which I strongly believe it will — the companies that control these private databases will dictate the terms of the new AI economy.

One company already holds a massive portion of the world’s most valuable private enterprise data. And right now, Wall Street is pricing it like a dying legacy business.

Oracle’s Position in AI Infrastructure

The company I’m buying is Oracle.

Before you roll your eyes at a legacy tech name, look at the actual data.

Last fall, Oracle nearly became a $1 trillion company. The catalyst? A massive deal with OpenAI to use Oracle’s cloud infrastructure. The market loved the narrative, and the stock soared.

Since that peak, the stock has been absolutely hammered. Over the last six months, the market has cut it nearly in half.

Oracle (ORCL) 12-month price action — stock down ~53% from September 2025 highs. Source: Yahoo Finance

Investors got nervous. They started questioning software companies in an AI world. They worried about spending. They worried about the balance sheet. They worried Oracle might be overbuilding infrastructure.

When the market smells uncertainty, it doesn’t stop to analyze the fundamentals. It just sells.

But the crowd is completely ignoring Oracle’s unique structural advantage.

if you like content like this and you like getting Trades that I am taking or looking at – you need to join my Black Ops Trading. For just five dollars you’ll get an entire year of access to me and my team including live mentoring sessions, newsletters, bonus reports and a ton more.

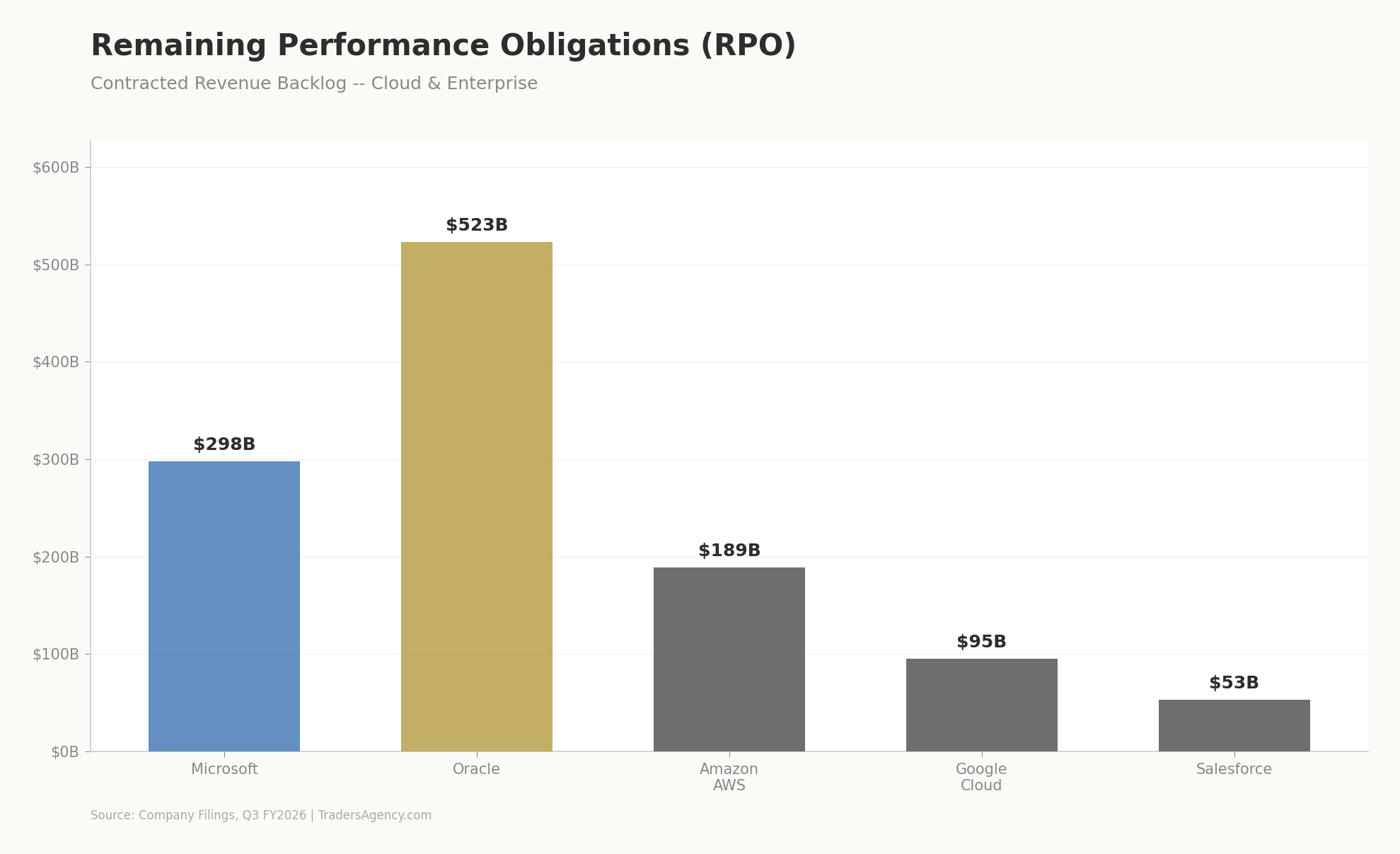

The $523 Billion Backlog Investors Are Ignoring

Oracle is now one of only a handful of hyperscale cloud infrastructure providers capable of supporting AI workloads.

Because Oracle came late to the cloud computing race, they actually ended up with a structural advantage. They didn’t have to retrofit old technology. They built their infrastructure specifically designed for AI training and inference.

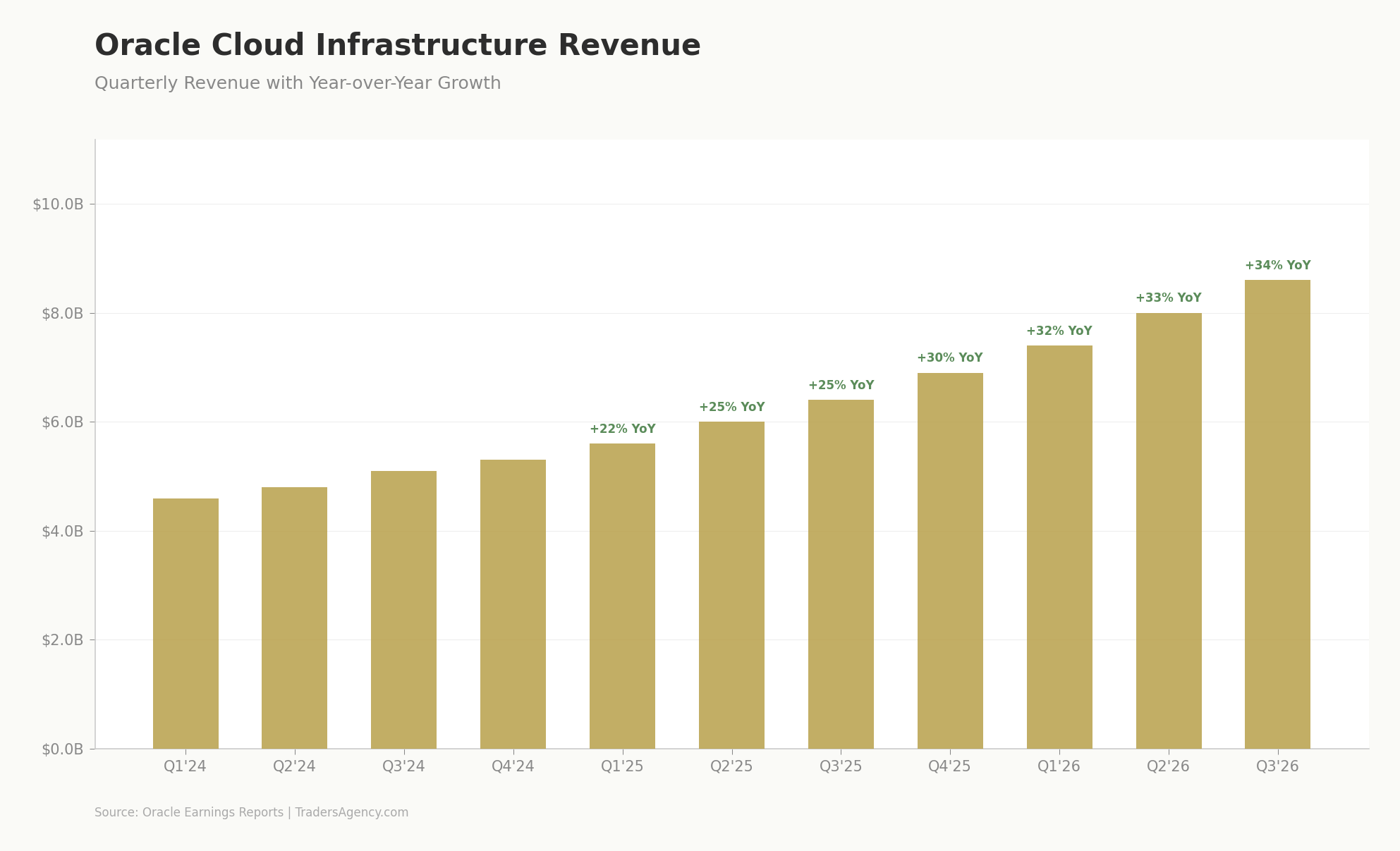

That’s why the underlying numbers are getting so compelling.

Oracle’s cloud infrastructure business is growing extremely fast. GPU-related revenue is surging. Broader cloud demand is exploding.

Yet the market is pricing the stock as if the entire growth story is broken.

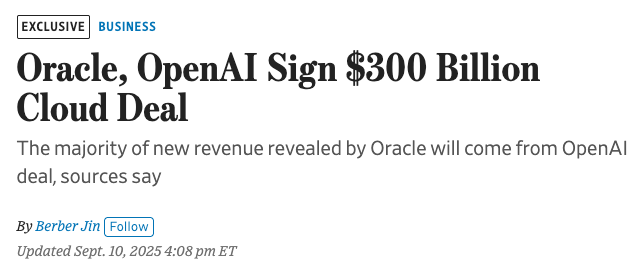

The $300 Billion OpenAI Deal

The sheer scale of Oracle’s contracted revenue is heavily tied to a contract that completely shocked the tech industry.

Oracle signed a $300 billion cloud infrastructure deal with OpenAI. That single contract represents a huge chunk of their overall backlog.

But there’s a specific catch — and it perfectly explains the current fear in the stock price.

This $300 billion deal doesn’t fully kick in until 2027. Oracle has to spend the money and build the physical infrastructure today to support that massive demand years down the road.

This gap between current capital expenditure and future revenue realization is exactly what’s terrifying short-term investors.

The AI Database 26ai Advantage

The real reason I’m positioning in Oracle goes far beyond cloud infrastructure. It comes back to Ellison’s strategy regarding private enterprise data.

Oracle recently launched something called AI Database 26ai. The concept is incredibly simple but highly disruptive.

Instead of taking private corporate data and using it to train an external AI model, you let the AI query your private data in real time. This technique is known as retrieval augmented generation. The AI doesn’t absorb the data into its core model. It simply reasons over it. The data never leaves the vault.

Think about the real-world applications:

- A hospital can analyze patient histories without ever exposing records

- A bank can evaluate loan portfolios without leaking customer information

- A defense contractor can run AI analysis on classified systems

If retrieval augmented generation becomes the dominant way enterprise AI operates, the companies controlling those enterprise databases suddenly hold all the power.

Oracle owns a massive portion of those exact databases.

The Risks Investors Should Know

I never enter a position without acknowledging the downside. The risks here absolutely exist.

Oracle is spending heavily to build out cloud capacity. That means taking on debt. It means burning cash in the short term. If demand doesn’t show up exactly as expected, margins could get pressured.

There’s also concentration risk. If OpenAI struggles or demand changes, that impacts Oracle more than some of the larger hyperscalers.

Real execution risk exists here. But as an investor, you have to ask one critical question when a stock drops 58%:

Did the actual business break, or did investor sentiment break?

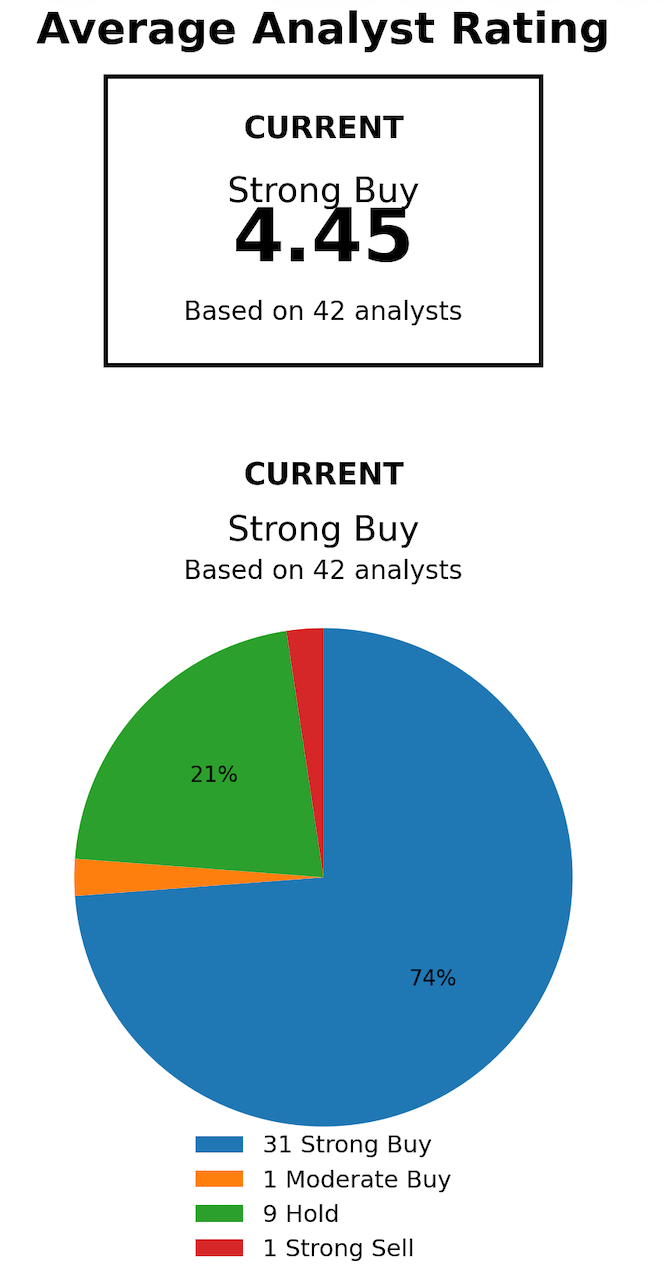

Wall Street’s Hidden Bullishness

While retail investors dump the stock, the smart money is quietly changing its tune.

Oppenheimer recently upgraded Oracle, suggesting the stock could gain roughly 25% from current levels.

Right now, the stock trades at roughly 22 times forward earnings. That’s cheaper than Microsoft. Cheaper than Amazon. Cheaper than Alphabet. Yet Oracle’s expected earnings growth is actually faster than some of those same trillion-dollar tech names.

That valuation disconnect is exactly what makes this setup so compelling.

How to Position

1. Ignore the Short-Term Noise

This is not a swing trade. This isn’t a typical short-term tactical setup. If you buy this expecting it to double next week, you’re playing the wrong game.

2. Play the Long Game

This is a longer-term positioning idea. You’re betting on the rise of enterprise AI over the next several years.

3. Focus on the Real Moat

You’re betting on private data becoming the actual, sustainable AI moat — not the commoditized public models. You’re betting that Oracle successfully executes its massive infrastructure buildout over the next several years.

Oracle might sound like a crazy stock to buy right now. It’s controversial. It’s been completely crushed. The market is full of doubt.

But the biggest opportunities in the market consistently show up exactly when everyone else stops believing in the underlying story.

Why Oracle Could Benefit From the Next Phase of AI

If Larry Ellison is right about the future of artificial intelligence, the entire market is currently looking in the wrong direction.

The next great AI battleground won’t be fought over who has the smartest public model. The models will all equalize.

The real battleground will be the data.

The companies that hold secure, private, enterprise-level data will dictate the terms of the next digital revolution. And if that happens, Oracle is sitting right in the middle of it — with half a trillion dollars in contracted revenue already locked in.

That is a setup I’m willing to buy.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I’ll see you in the next live session.

DISCLAIMER: Traders Agency does not offer financial advice. The information provided is for educational purposes only and should not be considered financial advice. Traders Agency is not responsible for any financial losses or consequences resulting from the use of the information provided. Trading carries inherent risks and may not be suitable for all individuals. You are advised to conduct your own research and seek personalized advice before making any investment decisions, recognizing the potential risks and rewards involved.