North American Construction Group Ltd.

North American Construction Group Ltd. (NOA) is an Acheson, Canada-based mining and construction services company focused on the resource development and industrial construction sectors in both Canada and the United States.

Formerly known as North American Energy Partners Inc., NOA operates two main divisions: Heavy Construction & Mining and Equipment Maintenance Services. At the end of 2020, the company had a heavy equipment fleet of 626 units.

Alberta is a primary resource province for Canada. It is ground zero for the tar sands oil as well as for numerous industrial and other ores and minerals. North American Construction Group contracts its equipment as well as its teams in various stages of initial, continuing and reclamation projects in various locales in and beyond its home province.

The company’s equipment is hard to replace these days – adding to its capabilities and contract sales compared to both its peers as well as companies that might ordinarily run their own equipment and services.

Resources, from oil to ores, are all in higher demand – aiding the company. And reclamation mandates make its services must have when fields and mines need to be retired.

Sales are up and are backed up by impressive operation margins that currently are running near 14%. And in turn, the company delivers an impressive return on its shareholders’ equity of near 23%.

Debts are higher given the structure of the company and the intensive capital requirements, but it is manageable with good cash flows under contracts.

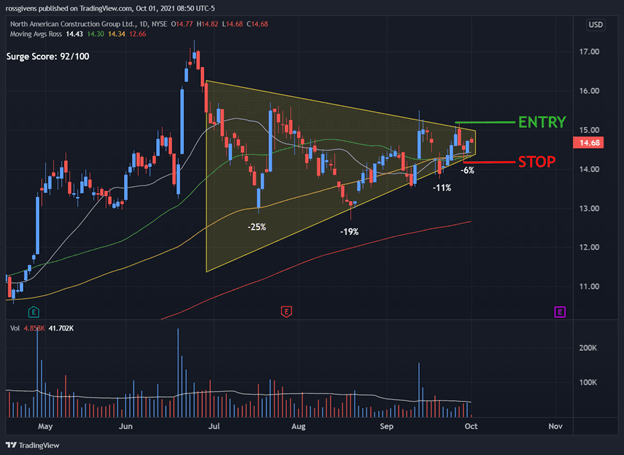

Here’s how the chart is setting up:

And here’s how the stock is setting up with my Stock Surge Indicator (SSI):

- Surge score: 92/100

- % Above 52-wk low: 145%

- MFI reading: 59

- Sales growth: +98%

- Triple momentum: yes

NOA stock has more than doubled over the last 12 months.

The share price then began to consolidate in July with a succession of shallower dips and tightening price action.

There are also notable dips in volume during this period, and the high-volume days came at support levels and strong buying days.

With the trading range down to just 6%, I would buy NOA on a move above $15.20 with a stop beneath last week’s low.

Opiant Pharmaceuticals, Inc.

Opiant Pharmaceuticals, Inc. (OPNT) is the Santa Monica, California-based specialty pharmaceutical company focused on developing medicines for addictions and drug overdoses.

Formerly known as Lightlake Therapeutics Inc., OPNT currently offers its NARCAN nasal spray as a treatment for reversing opioid overdoses, and it has several other product candidates in its pipeline that aim to treat opioid overdoses and disorders, alcohol use disorders and acute cannabinoid overdoses.

Addiction resolution and abatement unfortunately continues to be a major problem that in the US alone is on the rise. And insurance companies increasingly are also providing coverage – empowering victims with greater ability to get through and past their troubles.

In addition, government-sponsored programs are also strongly on the increase in their reach and capabilities – aided by recent legal settlements with specific drug manufacturers, distributors and pharmacies.

Like for other developmental drug and medical treatment companies, Opiant is focused on its new and pending products and building out its business. This means negative margins and losses for the near term. But this is all known by investors and financiers – and for now is not an issue.

Investors and funders are all focused on building up the company, including a potential further exit strategy that could be an eventual windfall. But for now, equity capital is ample, debts are well below stress levels and also at lower levels to its ample asset base including its patents and other intellectual properties.

Here’s how the chart is setting up:

And here’s how the stock is setting up with my SSI:

- Surge score: 99/100

- % Above 52-wk low: 277%

- MFI reading: 72

- Sales growth: +78%

- Triple momentum: yes

Opiant is currently maxing out my Stock Surge Indicator with a reading of 99/100. And it’s easy to see why.

This was an $8 stock last year that is now trading against resistance at the $26 level.

At a valuation of just $113 million, OPNT is a micro-cap stock. Most investors view this as “risky.”

But I see it as an opportunity to get in early on what could be a huge winning stock and company.

As you can see from the chart above, the stock price has stalled after making another huge surge last month.

Retracements have been capped at 11%, which to me is an acceptable risk for a stock with an SSI reading of 99 that is showing such breakaway strength.

Look to buy on a breakout above the $26 level.

Hollysys Automation Technologies Ltd.

Hollysys Automation Technologies Ltd. (HOLI) is a Beijing, China-based industrial automation solutions company focused on electrical equipment and parts.

HOLI offers a suite of industrial automation systems for the industrial, railway, subway, nuclear power and mechanical and electronic industries, hardware-centric products like actuators as well as software-centric distributed control systems.

Automation was a big deal even before the past years of labor shortages. Hollysys is a leader in this business segment that has other participants, but many of them are private providing investors in this company with a particularly attractive opportunity right now.

Sales are good, but operating margin is really good at 19.15% – impressive given the complexity of its manufacturing. The challenges right now include power supplies as China continues to limit industrial consumption as it catches up with fuel shortages for its major utilities that will be impacting this company.

Shipping is also a challenge for both supply-chain management for its own production as well as its shipping of finished products. But it has heavy government support that gives it a bit of an edge.

Debt is nearly nil, and good cash and credit capability is all in this company’s corner. And the shares are cheap as they trade now at a discount to its intrinsic (book) value by nearly 20% making for a big bargain right now.

This in turn is bringing in takeover deals that may bring a further gain in the shares in shorter order as the board of directors is evaluating various proposals for co-ops or a full deal for the company. This is not without some competition for the company and its assets. But for us – this is all good for the share valuation in the US market.

Here’s how the chart is setting up:

And here’s how the stock is setting up with my SSI:

- Surge score: 94/100

- % Above 52-wk low: 87.7%

- MFI reading: 59

- Sales growth: +36%

- Triple momentum: yes

Soon after confirming its uptrend in August, HOLI gapped up on news of a new acquisition offer.

There seems to be a race to take over this company, and a new suitor offered $23 per share – well above the $17.10 offer made by CPE Funds Management.

Bidding wars like this are always good for shareholders since a buyout offer will only be accepted at a price above current market value.

Based on the shallow retracements and HOLI drifting higher since the announcement, there doesn’t seem to be much doubt in the eyes of large investors.

If a new, higher offer comes in (or even the rumor of one), expect a breakout in HOLI that should be buyable.

Embrace the Surge,

See more from Traders Agency on Google

Make us a preferred source and our market analysis will appear more prominently in your Google Search, Top Stories, and AI results.

Add to Preferred Sources