The Inflation Narrative vs. Reality

The Federal Government and the Federal Reserve operate on narratives. Facts play a role, but policy decisions often hinge on the story central bankers want to sell. Right now, that story says inflation is cooling rapidly, paving the way for a shift in monetary policy.

A deeper look at the data reveals a sharp disconnect between headline numbers and the financial reality facing consumers and investors.

The most recent CPI report shows inflation has cooled to 2.4%. On the surface, this looks like a victory—approaching the Fed's long-standing 2.0% target. This low headline number provides the political cover needed to consider cutting interest rates again.

But relying solely on this figure ignores what's actually driving the index down. And more importantly, what continues to surge.

The current "cooling" is largely the result of a significant drop in energy costs. Gasoline prices are down approximately 8% year-over-year. Because oil is a major input cost for diesel fuel, transportation, and energy broadly, a drop in oil prices suppresses costs across the supply chain.

This decline has been the primary force keeping headline inflation at that palatable 2.4% level.

The Real Cost of Living

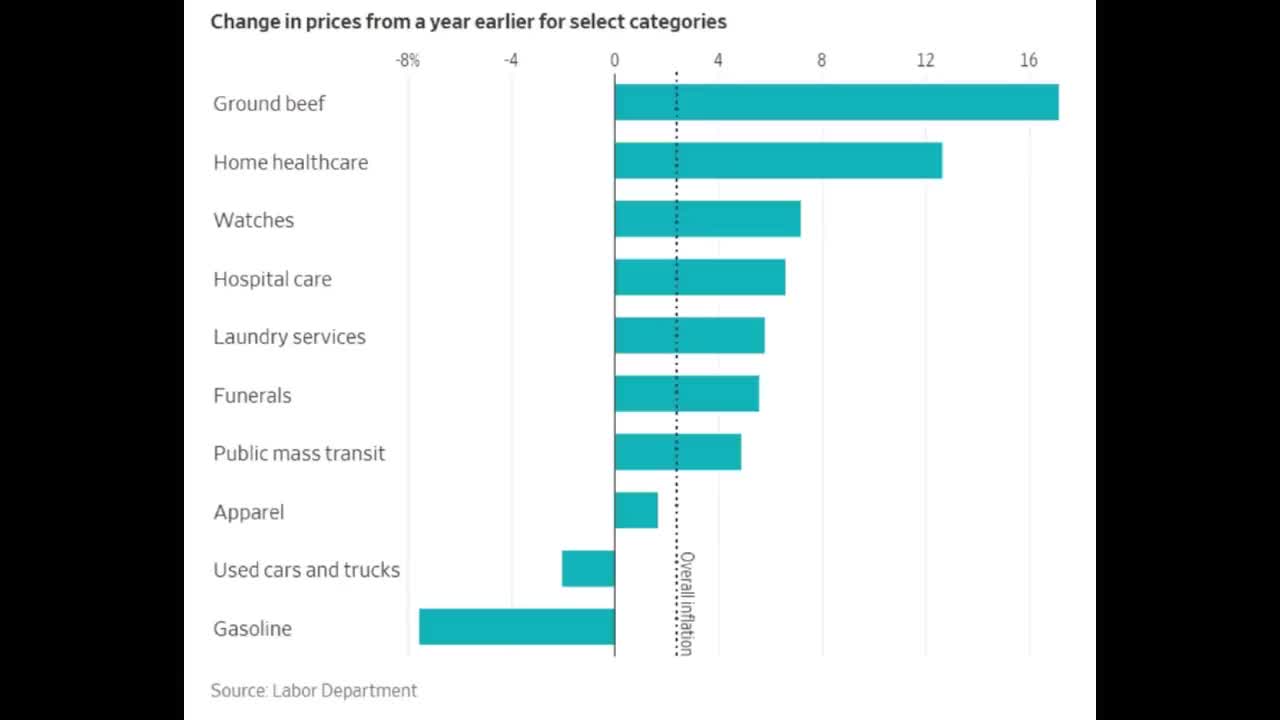

While energy prices have provided relief, other essential sectors show no signs of cooling. Strip away gasoline, and the year-over-year price changes for essential goods and services paint a much more aggressive picture.

The "cooling" narrative collapses when applied to the daily expenses that dominate household budgets:

- Ground beef: Up more than 16%

- Home health care: Up more than 12%

- Hospital care: Up 7%

- Funeral costs: Up 6%

- Public transit: Up 5%

These figures do not reflect an economy returning to a 2% baseline. Insurance costs and property taxes continue rising well above the headline rate. While the Fed cites 2.4% CPI to justify its policy stance, the reality for consumers involves double-digit increases in food and healthcare.

The Labor Market Problem

Typically, interest rate cuts are a tool used to stimulate a weak economy or halt rising unemployment. If the Federal Reserve were acting solely on labor market data, there would be zero justification for lowering rates in the immediate future.

The economy added 130,000 jobs in January, smashing expectations. More importantly, the unemployment rate is trending downward, not upward.

The trajectory over the last three months tells the story: November at 4.6%, December at 4.4%, January at 4.3%.

The labor market is solid. It does not need saving.

Since the "save the jobs" argument is invalid, the narrative has pivoted back to inflation. The argument is now that because inflation is ostensibly low at 2.4%, the central bank can "afford" to cut rates. This shift is critical for investors to recognize—rate cuts are coming regardless of whether the economy actually needs them.

The Rate Cut Timeline

The market is pricing in a specific timeline for rate cuts, and it aligns perfectly with the expected change in leadership at the Federal Reserve.

For the upcoming meeting on March 18th, the CME FedWatch tool shows a 90.2% chance the Fed will not cut rates. This aligns with Jerome Powell's current stance—he's unlikely to lower rates simply to appease political pressure.

Looking ahead to April 29th, the probability of rates remaining unchanged sits at 71.5%. This marks the final FOMC session with Powell as Chair. The market expects him to hold the line until his departure.

Then the calculus changes dramatically.

The June Shift

President Trump's most likely new Fed chair nominee, Kevin Worsh, is expected to come into power in the middle of May. The next Federal Reserve meeting after April is scheduled for June 17th.

The probabilities flip aggressively:

Why do the odds swing from a 71.5% chance of holding steady in April to a 68% chance of cutting in June? The market believes the new Fed Chair will do President Trump's bidding and cut interest rates.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading Club

Fed Independence Is Over

The market believes that the Federal Reserve is no longer independent of the US government, not even for optics. Investors believe the new Chair will execute the monetary policy desired by the executive branch.

President Trump has made it clear he favors lower interest rates. It stands to reason he would select a nominee willing to execute that vision.

A straightforward political calculation: a President would not hire a candidate who refuses to listen to policy preferences when other candidates are available who will. The market is pricing in the assumption that Kevin Worsh will do President Trump's bidding.

For investors, this signals a transition in monetary policy. When the central bank prints money or cuts interest rates, it generally provides a tailwind for assets like stocks and precious metals.

But this rising tide will not lift all boats equally.

AI Disruption Changes Everything

While lower interest rates generally support equity valuations, specific structural challenges in the technology sector may outweigh the benefits of cheaper capital. The rise of AI is creating a new era of winners and losers.

The critical question: Which companies will become obsolete due to AI, and which stand to benefit?

Interest rate cuts cannot save a company whose core business model is being rendered obsolete by superior technology.

The Duolingo Problem

Duolingo, the language learning platform, has suffered significantly. The company charges approximately $12 a month for its premium service.

In an era of advanced AI, this value proposition is questionable.

Users can now utilize platforms like ChatGPT to perform the same functions for free or as part of a broader subscription. AI can provide daily vocabulary words, correct grammar instantly, teach correct pronunciation, generate specific cultural nuances like phrases specific to Colombian Spanish, and create distinct lesson plans covering common slang in Mexican Spanish.

An AI platform can do all of this cheaper and better than the paid Duolingo application. Duolingo lacks a moat—a defensive barrier protecting its business.

Interest rate cuts may not be enough to offset the impact of AI disruption. Monetary easing cannot fix a broken business model.

Amazon's Physical Moat

Contrast a vulnerable software company with a giant like Amazon. Amazon's stock is down 12% over the past one year as the market attempts to figure out how AI impacts various sectors.

But Amazon possesses a defensive characteristic that purely digital companies lack: a physical moat.

Amazon is already utilizing AI to make its operations more efficient. Its true defense lies in the physical world. AI software cannot magically deliver products to a doorstep, magically create physical warehouses, or replace a logistics network of trucks and airplanes.

Even if a competitor uses AI to build a better shopping interface, they still face the hurdle of replicating Amazon's logistical and physical infrastructure. Amazon has trucks, airplanes, warehouses, and inventory networks.

This physical reality provides a layer of protection against AI disruption. Interest rate cuts will be a tailwind for stocks, but in certain industries, that may not be enough to offset specific challenges or disruption.

The Gold Setup

While the outlook for individual stocks varies based on AI disruption, the outlook for gold appears much clearer. Gold is already getting a tailwind from de-dollarization—other countries preferring gold as a reserve asset. And interest rate cuts will be another tailwind for gold.

The relationship between interest rates, inflation, and gold is mechanical:

Gold is facing a situation where it's getting tailwinds from de-dollarization, a tailwind from money printing, and soon a tailwind from lower interest rates.

Positioning for the Pivot

The economic data presents a conflicting picture: a strong labor market with falling unemployment at 4.3% and "cooling" headline inflation at 2.4%, contradicted by surging prices in beef, healthcare, and insurance.

This is setting the stage for President Trump's new Fed chair to cut interest rates.

The market is signaling that the current Federal Reserve Chair will hold rates steady through April, but the incoming leadership is expected to cut rates by June. This expectation is driven by the belief that the new regime will prioritize rate cuts regardless of labor market strength.

Investors should not be lulled into a false sense of security by the broad assumption that rate cuts help all stocks. AI disruption remains a potent force that can dismantle companies with weak moats, regardless of the interest rate environment.

But for assets like gold, the combination of de-dollarization, money printing, and imminent rate cuts creates a favorable setup.

Get an entire year of live weekly mentoring sessions, my newsletter, indicators, bonus reports, tons more. Click the link and I'll see you in the next live session.

Join my Black Ops Trading ClubDISCLAIMER: This content is for informational and educational purposes only. It should not be considered tax, financial, or legal advice. Consult a qualified professional for advice specific to your situation. Trading carries inherent risks and may not be suitable for all individuals.